How do Hospitals Compete with Free Standing Clinics?

How do Hospitals Compete with Free Standing Clinics?

The continued pressure on shoppable services has heightened the competition between hospitals and freestanding facilities. But what effect does this have on their day to day business? We analyzed the rate at which hospitals and their freestanding competitors have increased charges in four key groups from 2015 to 2019: imaging, procedures, labs, and therapies and found some interesting trends!

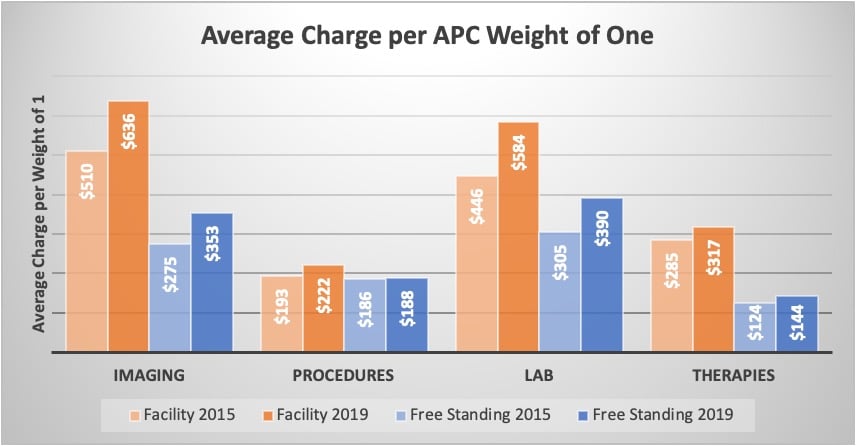

The chart below compares U.S. averages from Medicare data for 2015 and 2019. To account for the difference in charges due to case mix, we have adjusted procedure prices by their Medicare Ambulatory Patient Classification (APC) relative weight. We mapped the HCPCS to the appropriate group, calculated total charges and total APC Relative Weight (RW), and finally divided total charges by total RW to arrive at the average charge per RW of one.

In imaging, we see hospitals have slightly closed the gap, increasing their average charge by 25% compared to 29% at their freestanding counterparts. This is a small difference and suggests that hospitals may not believe price elasticity in this area is very high and they are willing to maintain a price premium.

Looking at procedures, hospitals have increased their average charge by 15% compared to 2015, as opposed to ambulatory surgical centers where the rate of increased remains nearly flat at 1%. It should be noted that while the average charges in this area look competitive between hospitals and ASCs, hospitals often do not include surgical supplies or anesthesia in their pricing for procedures. This differs from ASCs where the price is more inclusive. The relatively low rate of increase for ASCs (1%) suggests that ASCs may see little association between price and net revenue, or they may perceive a highly competitive price market with hospitals.

Labs are moving at similar rate of increase with hospitals increasing their average charge by 31% compared to 28% at the freestanding facilities.

When looking at therapies, hospitals are closing the gap with freestanding facilities, increasing their charges by 11% compared to 16% at the freestanding sites.

The critical question for healthcare providers in these four outpatient service areas is to what extent does price drive market share? In the four areas that we reviewed, the relative difference between hospital and free-standing prices remained relatively constant. Only in the procedure area was there a significant variance between hospital and free-standing price changes which may suggest market stabilization in these areas. Price transparency could provide some significant future price movement as hospitals modify prices to enhance their relative marketplace image.

Is your facility interested in understanding your pricing position relative to freestanding competitors? We can help!

Have thoughts or questions?

Related