Is Die Hard a Christmas movie? Obviously. Is it the greatest Christmas movie? Well, that’s up for debate. We’ll let your holiday dinner table take up that one.

But we at Cleverley + Associates can weigh in where we’re experts, which is hospital pricing data! Action movies, especially one as hard core as Die Hard, mean injuries and injuries mean hospitals. Sure, John McClane pulled away in style as the music swelled, but we assume his wife talked him into going to an ER to at least make sure he wasn’t still bleeding.

Our first injury is fist-fighting-while-falling-down-the-stairs. There are a lot of injuries that can occur from both a fall and a fight, but since Mr. McClane goes on to punch several other people, we can rule out fractures, spinal injuries, or any injury major enough to take McClane out of the fight.

He’d probably get an MRI and CT scan (Let’s go ahead and do both, since he’s a hero.)

We’d also want to do an ImPACT test.

Here’s what the prices looked like for the last few years. While an MRI will cost Mr. McClane more this year, he’ll save some money on the ImPACT test.

Next, our hero cuts his feet on broken glass. (OW! OW! OW!)

We’re going to need a lot of antiseptics, bandages, and probably stiches. Also, foreign body removal from the wounds.

Again, ow.

It looks like, overall, it’s going to be cheaper this year! Good news! Flex those toes!

Next up, poor McClane is shot in the shoulder! The following scenes, where he still manages to win in hand-to-hand combat with the villain, show that the bullet likely grazed him. Of course, we can’t rule out that the bullet is still there, or a shard of it. So, we’re going to have to explore the wound to make sure it’s clean, and probably take an x-ray to make sure we got all the bullet bits out.

It’s going to be more expensive this year.

Lastly, in the grand finale, John McClane wraps a fire hose around himself and bungee jumps off the building. This is, generally speaking, a terrible idea. He then breaks through a window using his already battered body. Again, do not try this at home…or in an office building.

This could, of course, cause a variety of injuries, but let’s go ahead and just assume the worst – a fracture of the vertebrae and ribs. There would probably also be internal damage as well, but considering he’s still walking around being witty, let’s assume he’s miraculously okay-ish.

The end of the movie seems to suggest that McClane rides off into the sunrise with his wife, triumphant and filled with the Christmas spirit. I assume they didn’t go straight home with the hope that he would survive until morning. More likely they stopped at the ER to at least make sure he wasn’t on death’s doorstep.

Happy Holidays everyone! Yippee-ki-yay!

Would you like to know how well your hospital measures up if an action hero appears in your facility? We can help!

CMS CY22 OPPS Final Rule – Points To Know About Price Transparency

To encourage hospitals to comply CMS has dramatically increased the penalty for non-compliance. Beginning January 1, 2022, CMS will increase the penalty for some hospitals that are found to not be complying.

Standard Machine-Readable File Recommendations for Hospitals

The CY22 proposed rule covered many topics, but, in our opinion, the guidelines and clarifications surrounding machine-readable files were some of the most critical.

The Proposed Rule’s observation that there was a “lack of uniformity in the way that hospitals display their standard charges (84 FR 65556)” wasn’t a great surprise to the industry. The original guidelines required certain data elements but did not specify an exact file structure. Hospitals naturally constructed a file that best fit their data, but these files could be difficult to compare from one hospital to the next.

CMS has been very clear that its goal is to make the data as accessible to the public as possible, so it’s understandable that they saw clarification in this area as a priority. We believe CMS is right that there is a wide variety of file structures out there, and that makes it hard to meaningfully compare hospitals. Our research shows a few challenges to fixing this particular issue.

First is the presence/updates of information. How do we locate and download the files? This issue will improve once hospitals use the CMS naming convention for machine-readable files. Another solution would be for CMS to define “prominently displayed” as requiring two clicks from the hospital or health system home page.

The next challenge is file type and layout difference. There’s a lot of variation between hospitals and systems. Requiring the same file type and standardizing the structure, as well as defining the data elements, could resolve this and will help create a national database.

Relational differences are another hurdle. Hospitals sometimes report payer-specific negotiated charges with HCPCS, MS-DRG, APC, per diems, case rates, and charge codes. This variation can be solved by creating a standardized display.

Payer naming differences also cause issues since there are no standardized naming conventions. Again, a uniform structure can solve this issue.

To this end, we have constructed a proposed standardized single machine-readable file. In December 2019, CMS stated that a single machine-readable file could have different sections but needed to contain all required elements. Here’s how each section could be defined to allow for uniform reporting. What follows is a summary of our recommendations. You can find a more detailed description here.

Section One: Gross Charge Information

This includes six fields. The primary comparison link is CPT®/HCPCS; revenue codes can also be compared on a more manual basis through item descriptions, as well (useful for room rates and operating room associated codes, as primary examples).

Section Two: Discount Cash Price Information

Not all hospitals have established their cash pay policies in the same way. To account for this variation while still permitting standardized reporting, we believe the “Discount cash price” section should have two options, Policy and Price List.

Policy – a text field for an explanation of the hospital’s policy, how it is applied, and contact information for financial assistance.

Price List – for hospitals with an established price list, information could be displayed in the same format as the Gross Charge display.

Section Three: Payer-Specific Negotiated Charge

This is the area that contributes most to the lack of consistency within the files. There is an incredible amount of variability. It is very difficult to compare payers and plans from one hospital to another. Here is how we propose tackling it.

Standardized Payment – Unless all payers utilize the same payment methodologies it isn’t possible to look at payment differences. Standardized payment rates and utilization must be considered in order to understand payment differences. CMS has established payment systems for inpatient and outpatient claims that are utilized by all hospitals subject to the transparency reporting requirements. The solution to standardizing disparate payment systems is for hospitals to determine how the claim would be paid using the specific payer negotiated contractual language and then reported under Medicare-based grouping logic by MS-DRG (inpatient) or primary APC (outpatient). The steps to do this, are:

Derive expected claim payment for all items and services based by consulting the negotiated rates and terms with the specific payers. This would be done for all claims – not using historical reimbursement – but a calculation of payment using current payment terms and rates.

Determine the MS-DRG (inpatient) or primary APC (outpatient) assignment for the particular patient claim. Grouper logic is quite common for hospitals and many already run every claim through Medicare logic to determine a MS-DRG assignment. Each claim would be labeled with a MS-DRG or primary APC designation (more on outpatient grouping later).

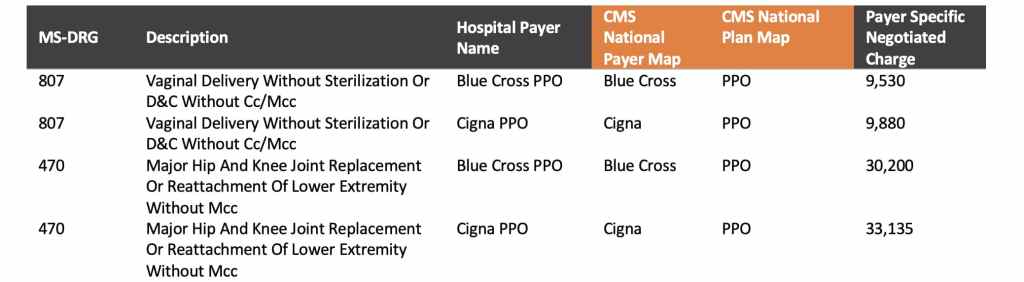

Report the standardized payer-specific negotiated charge by MS-DRG or APC for all required payers in a simple format illustrated below. This display would encompass all items and services and service packages and would also be representative of service utilization – the critical element needed to understand payment differences.

Again, further details can be found here. Hospitals could derive the payer-specific negotiated charges with their contracted rate sheets and terms and applying those to actual patient claims. Without patient claim detail the hospital cannot satisfy the requirements of the rule because the number of combinations of items, services, and service packages is nearly limitless on a per-patient basis.

Standardized Payer Mapping – Once payment has been standardized, payers must be compared through common mapping. CMS could create a list of national/regional payers and the hospitals could link to that. This map could be for the top twenty or thirty payers and would allow for easier comparisons.

Standardized Reporting Structure – Here is a simple, standardized format that would accommodate these needs.

Section Four: Payer-Specific Negotiated Charge

The benefit of using the structure identified in Section Three is that minimum/maximum values are very easy to present. A researcher could easily calculate minimum, maximum, and other statistical measures based on the standardized data format presented. Still, this information could be compiled like this:

We believe that if the CMS seeks to standardize the Machine-Readable File it should do so in a way that will meet current requirements while providing meaningful information. The structure we have proposed addresses these requirements and solves for the challenges that stakeholders are experiencing with current disclosed data.

Are Hospitals Really Flouting Federal Requirements?

A new report by PatientRightsAdvocate.org claims that only 5% of US hospitals are fully compliant with disclosing their prices as required by the CMS. A summary of their report was featured in The Washington Post and has brought several questions from hospitals around the country. You can read The Washington Post article here.

We took a close look at the report’s findings and concerns – and have put together our own observations and considerations.

First, we find the overall compliance rate of 5% exceptionally low. While there has been agreement that hospitals have not fully complied with all aspects of the new requirements, this research seems particularly biased and had a lower sample size of 500 hospitals. Our own research found 29% compliance when evaluating approximately 3,400 hospitals. We believe our compliance rate aligns with other national organizations evaluating the transparency disclosures. For example, other key research groups found the following compliance rates:

Kaiser = 33%

Health Affairs = 22%

Milliman = 68%

Guidehouse = 45%

The report says, “We identified a hospital as noncompliant if it omitted any of the five standard charge criteria required by the rule, if it posted blanks or zeros in the data fields, if it did not post all negotiated payer rates associated with specific plans, or if the price estimator tool did not show both the negotiated rates and discounted cash prices to provide pricing for all healthcare consumers, including the uninsured and those desiring to pay cash directly.” However, there are several flaws with this approach:

Discounted cash pricing – some hospitals do not have established cash-pay prices. While CMS requires this to be posted if the hospital has developed cash pricing, this group should not assume the exclusion of this information means the hospital has determined not to post it. In CMS hospital audits, if this data is not present CMS has asked for validation. We believe best practice would be to disclose if this pricing has not been developed to avoid confusion. Still, an assumption of guilt is not fair and is a contributing factor to the lower overall compliance rate.

Blanks/Zeros in data fields – there are numerous examples where a hospital could have a zero or null value for standard charge elements. Again, to assume that the hospital is non-compliant for this reason alone is outside of the CMS requirements and does not reflect an understanding of industry practices. Further, some examples of “compliant” hospitals on their list contained these values in their files. This inconsistency in review casts a large shadow on the credibility of the report.

Payer/Plan – the report found the biggest issue in this piece that “403 hospitals (80.6% of the 500) did not publish payer-specific negotiated charges ‘clearly associated with the names of each third-party payer and plan’ as required by the rule.” However, their review of the files again appears to be lacking industry knowledge. We see from their list of noncompliant hospitals that it appears they have assumed that all hospitals will have multiple negotiated rates for each payer. While this is common it certainly can’t be assumed to exist for ALL payers. The rule requires NEGOTIATED rates to be disclosed. So, if there is only one Aetna plan that has been negotiated than the hospital would only need to list Aetna once. This group seems to be assuming noncompliance based on not finding multiple entries for Aetna.

At the end of the day, the only group judging compliance that truly matters is CMS. While there is still some ambiguity around who CMS has deemed compliant in their reviews we do know that some of the elements this group has utilized do not align with the CMS requirements. Our opinion is that this report was primarily created to generate a headline and to promote their four proposed actions:

Stricter penalties for noncompliance and vigorous enforcement of the rule

Enhanced requirements for the list of 300 shoppable services

Requirements for actual prices, not estimates **Here the group would like to see guaranteed price quotes instead of price estimates in the shoppable tool

Requirements for clear pricing data standards

As for these four proposed actions, stricter penalties could be on the way due to language in the OPPS proposed rule. We also believe CMS will standardize reporting requirements in the future as this was also brought up for comment in the proposed rule. As for requiring price guarantees, hospitals are essentially doing this through many shoppable tools today. We’re not sure if this group is unhappy with the legal language that many tools have suggesting that a patient’s experience at the hospital could require care outside of what is being presented in the results? To convey patient care variability, our tool provides ancillary procedures that are commonly done in conjunction with the selected service and how that would impact their financial obligation. We believe this approach covers the needs of the hospital and the patient.

In sum, we find the report to be lacking industry experience, inconsistent in its application of review criteria to the sample, and intended primarily to paint hospitals in a negative light with proposed actions that are already being considered or implemented. If you have additional questions on price transparency you can watch our free summit here, or contact us here.

Hospitals Complying to CMS Price Transparency Requirements

We conducted a survey of hospitals and took a close look at their approaches to the new Price Transparency requirements. Here’s what we found.

Our Methodology

A breakdown of our research group, 137 health systems with 10+ hospitals.

Our research reviewed 137 health systems with 10+ hospitals within the health system itself, which represented 3,358 hospitals in total. We used the health systems webpage and their search engines to look for the Price Transparency files. We searched basic keywords such as machine readable, pricing transparency, pricing, standard charges, and charges.

Of those 137 health systems we found that 100 of them offered a dedicated system level website for pricing transparency. Our observations for the two reporting requirements – a machine-readable file and a consumer-friendly disclosure are as follows:

Machine Readable Results

Our major finding was that 40 of these systems met CMS’ Price Transparency requirements, meaning their files included all of the required charge criteria. Of the 137 health systems, we did find significant variation in what standard charge elements were being disclosed:

85% represented the gross charges within their machine-readable file

48% provided the discount cash price policy

40% provided the deidentified MIN/MAX values of the payer-specific charges

36% disclosed payer-specific charges

15% did not post any information at all

We only found 4% of those files represented some level of employed professional charges. This may be because there is still some confusion as to the definition of employed within the rule.

Components disclosed in the files

File Types (this is going to be a sub heading in the final)

We also found that there’s wide variation as far as what file types hospitals are using to display their Price Transparency information. The types of files used in posting the transparency files were:

38% Excel,

28% CSV,

12% JSON

11% Web/Tool

8% TXT

3% XML

Congress recently sent a letter to the Department of Health and Human services calling out format specifically. They wrote, “some hospitals… are providing the data in a non-usable format or failing to provide codes for items and services.” We believe CMS could be referring to that 11% of hospitals using the web tool format as cause for their concern.

Consumer Shoppable Results

Of the 137 systems we looked at, 119 of them disclosed information for the consumer shoppable requirement using either a web-based tool (113) or a downloadable file (6). Of the 119, we found that 15 likely would not be deemed compliant by lacking an uninsured option or creating some significant barrier to access. Per accessibility, we found 90% of all web-based tools used CAPTCHA security coding, and several facilities had a member login as well as a guest user access for the tool itself. MyChart used this particular strategy. Many web tools asked for emails, but only a few required it. As far as the spirit of the rule, the goal should be to make the information accessible as possible to the customer, with the fewest barriers to entry. In general, accessibility was something addressed in the CMS CY22 OPPS Proposed Rule which contained additional transparency comments. You can find our summary of the transparency components of the rule here.

Language and Authorizations

In nearly half of the hospitals we looked at, the disclosures were behind some kind of authorization or use-agreement. We had to agree that we understood their terms before we could see the data. In one case, a health system made the user watch a video on the CDM and how pricing is determined before the user was able to access the file. Some hospitals included language urging patients to reach out if they did not understand the information provided or the format of the data.

It is clear that many hospitals and systems are concerned that patients may not fully understand the data, or be able to navigate it with confidence, and are worried that these patients will make a complex decision about their medical care on this limited understanding. For this reason, these disclaimers may be helpful, though we don’t know how patients react to this language or if they integrate it into their decision-making process.

As more hospitals become compliant and researchers aggregate data, we look forward to getting a better perspective on all these issues.

Summary

Our review suggests that a more limited number of hospitals/health systems are complying with the full set of machine-readable requirements (29%) but a far greater number are disclosing consumer shoppable information (87%). The CMS CY22 OPPS Proposed Rule (summary here), seeks to increase the number of compliant hospitals by significantly raising the civil monetary penalties associated with non-compliance.

If you have questions about your hospital’s strategy, please contact us here! If you would like to see a deeper dive into this data, and all our research on Price Transparency, check out our Spring Summit here.